Introduction

The lending industry stands at a pivotal crossroads where traditional manual processing methods increasingly give way to sophisticated artificial intelligence-driven solutions. This transformation isn't merely about automation; it represents a fundamental shift in how financial institutions approach risk assessment, customer service, and operational efficiency. The integration of AI technologies into loan processing workflows has emerged as a critical differentiator for forward-thinking financial institutions seeking to maintain competitiveness in an increasingly digital marketplace.

Traditional loan processing, characterized by manual document review, lengthy verification procedures, and time-consuming risk assessments, typically requires days or even weeks to complete. This extended timeline not only impacts customer satisfaction but also increases operational costs and reduces the lending institution's market responsiveness. In an era where customers expect near-instantaneous service across all digital touchpoints, the ability to process loans rapidly while maintaining robust risk management has become paramount.

The Current Landscape of Loan Processing

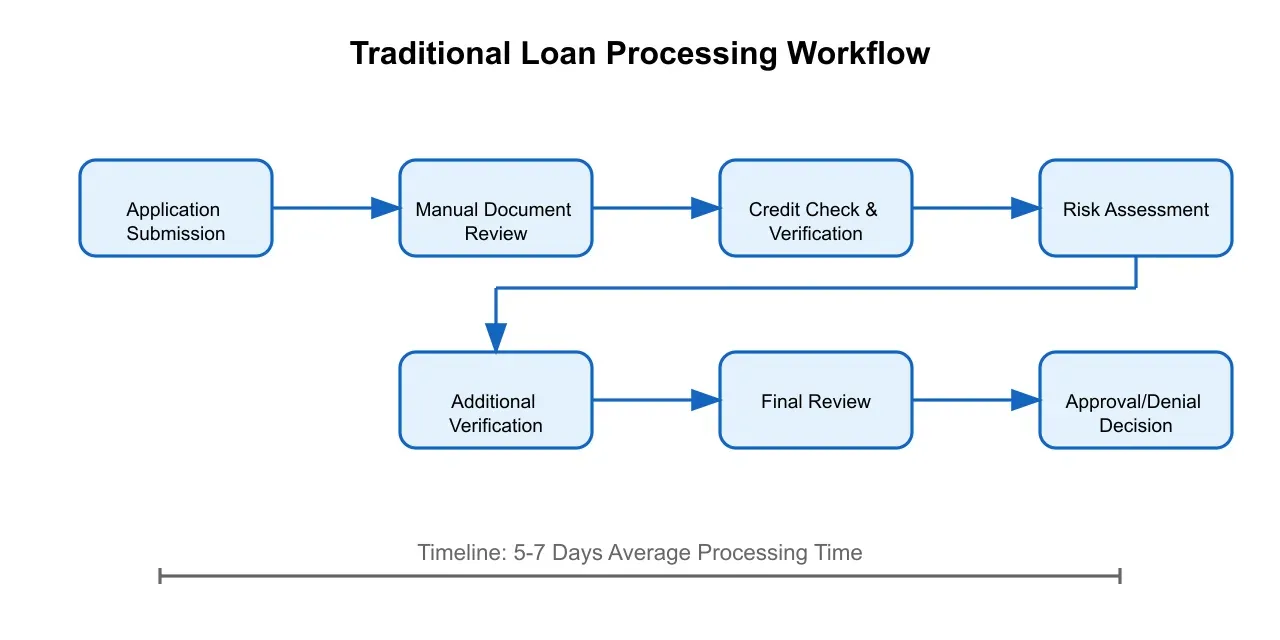

The traditional loan processing workflow encompasses multiple stages, each presenting its own set of challenges and inefficiencies. Loan officers must manually review extensive documentation, verify applicant information across disparate systems, and assess risk factors through time-consuming analyses. Figure 1 illustrates the conventional loan processing workflow, highlighting the numerous touch points and potential bottlenecks that contribute to extended processing times.

Research indicates that financial institutions spend an average of 5-7 hours processing a single loan application, with complex cases requiring substantially more time. This manual approach leads to several critical issues:

First, the substantial human involvement in document processing introduces a significant margin for error. Studies have shown that manual data entry in financial services has an average error rate of 3.6%, with each error potentially causing cascading problems throughout the approval process.

Second, the time-intensive nature of manual processing creates substantial opportunity costs. While loan officers are engaged in routine document review and data entry tasks, they have limited capacity to focus on high-value activities such as relationship building and complex case analysis.

Third, the inconsistency in processing times and decision-making criteria can lead to customer dissatisfaction and lost business opportunities. In a market where 68% of loan applicants cite processing speed as a crucial factor in choosing a lender, institutions that cannot offer rapid decisions risk losing market share to more technologically advanced competitors.

The AI Revolution in Loan Processing

The integration of artificial intelligence into loan processing represents a paradigm shift in how financial institutions approach this critical business function. AI-driven solutions, particularly those leveraging machine learning and natural language processing, can dramatically reduce processing times while improving accuracy and consistency in decision-making.

Modern AI systems can process and analyze vast amounts of structured and unstructured data in seconds, performing tasks that would take human operators hours or days to complete. These systems excel at:

Document Analysis and Verification: Advanced optical character recognition (OCR) combined with natural language processing can extract and verify information from various document types with accuracy rates exceeding 95%. This capability alone can reduce processing time by several hours per application.

Risk Assessment: Machine learning models can analyze hundreds of variables simultaneously, providing more nuanced and accurate risk assessments than traditional scoring methods. These models can identify subtle patterns and correlations that might escape human analysts, leading to more informed lending decisions.

Fraud Detection: AI systems can cross-reference application data against multiple databases in real-time, flagging potential fraudulent activities with remarkable precision. This enhanced security layer protects both the institution and legitimate applicants while maintaining processing speed.

Implementation Framework for AI-Driven Loan Processing

The successful implementation of AI-driven loan processing requires a structured approach that addresses both technical and organizational considerations. Financial institutions must carefully orchestrate the integration of AI systems while maintaining regulatory compliance and ensuring seamless operation with existing infrastructure.

Technical Architecture and Integration

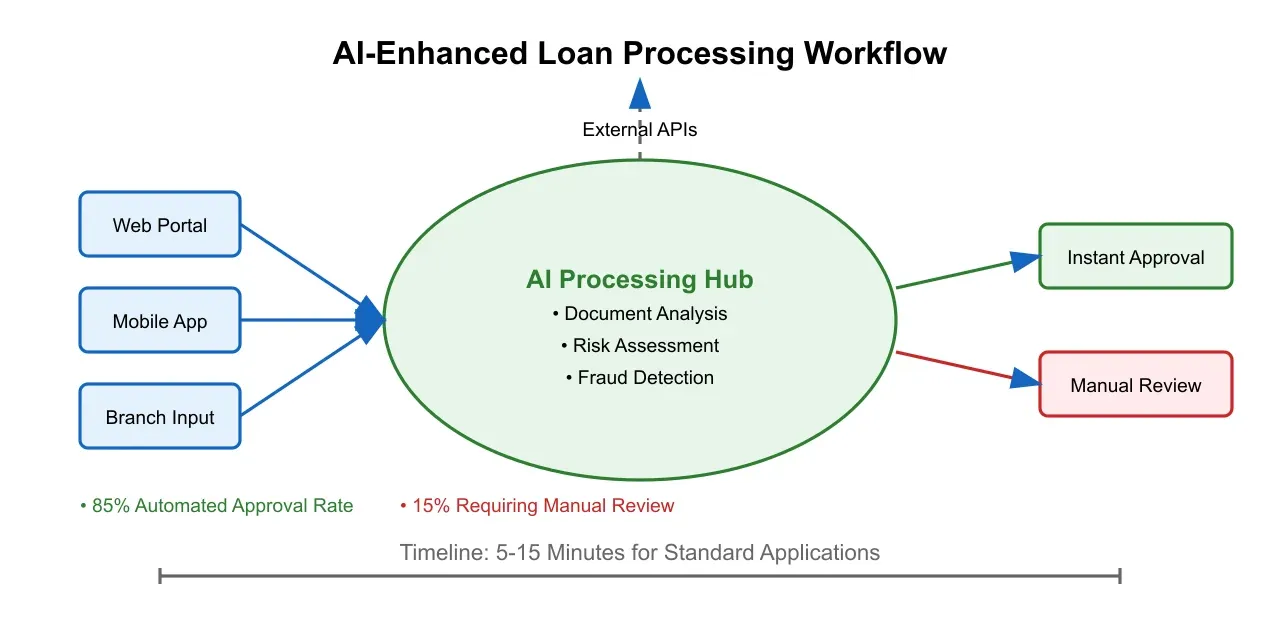

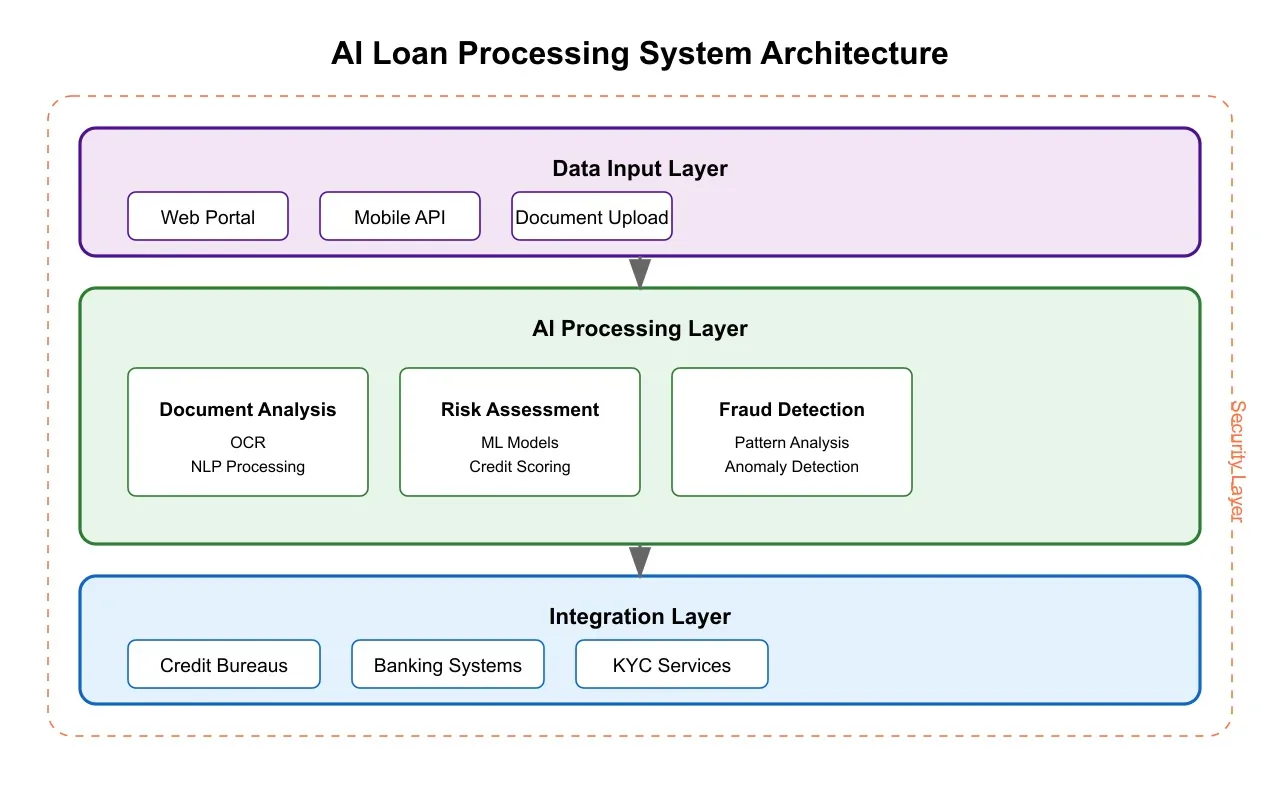

The foundation of an AI-driven loan processing system rests upon a robust technical architecture that facilitates seamless data flow and processing. Figure 3 illustrates the key components and their interactions within a modern AI-powered loan processing system.

At the heart of this architecture lies a sophisticated data pipeline that handles both structured and unstructured information. The system begins with multiple input channels, including web portals, mobile applications, and traditional paper documentation, all feeding into a centralized processing hub. This hub employs several key technologies:

Document Processing Engine: Advanced OCR and computer vision technologies process incoming documents, extracting relevant information with high accuracy. Modern systems achieve recognition rates exceeding 98% for standard financial documents, significantly reducing manual review requirements.

Data Verification System: AI algorithms automatically cross-reference extracted information against multiple databases, including credit bureaus, public records, and internal datasets. This parallel processing approach reduces verification time from hours to minutes.

Risk Analysis Module: Machine learning models analyze applicant data using both traditional metrics and alternative data sources. These models continuously learn from outcomes, improving their predictive accuracy over time. Research indicates that AI-driven risk assessment can reduce default rates by up to 25% compared to traditional scoring methods.

Regulatory Compliance and Risk Management

The implementation of AI in loan processing must carefully balance automation with regulatory compliance. Financial institutions must ensure their AI systems adhere to various regulatory frameworks, including:

Fair Lending Requirements: AI models must be regularly tested for bias and discrimination, with particular attention to protected classes under fair lending laws. This includes implementing robust monitoring systems that track decision patterns and flag potential disparate impact issues.

Data Privacy and Security: With the increasing focus on data protection regulations such as GDPR and CCPA, AI systems must incorporate privacy-by-design principles. This includes end-to-end encryption, secure data handling protocols, and comprehensive audit trails.

Explainability Requirements: Regulatory bodies increasingly require that AI decisions be explainable and transparent. Modern systems incorporate explainable AI (XAI) techniques that provide clear rationales for lending decisions, helping satisfy both regulatory requirements and customer expectations for transparency.

Performance Metrics and Business Impact

The implementation of AI-driven loan processing systems has demonstrated remarkable improvements across key performance indicators. A comprehensive analysis of institutions that have adopted these systems reveals:

Processing Time Reduction: Average loan processing times have decreased from 5-7 days to less than 24 hours, with simple applications often completed in minutes. This dramatic improvement directly impacts customer satisfaction and competitive positioning.

Cost Efficiency: Operational costs associated with loan processing have decreased by an average of 40-60%, primarily through reduced manual labor requirements and improved process efficiency. This cost reduction enables institutions to offer more competitive rates while maintaining profitability.

Error Rate Reduction: Manual processing errors have decreased by over 90%, leading to improved compliance outcomes and reduced costs associated with error correction. The standardization of processing through AI has virtually eliminated common issues such as missing documentation and incorrect data entry.

Customer Satisfaction: Net Promoter Scores (NPS) for institutions implementing AI-driven loan processing have shown average improvements of 25-30 points, primarily attributed to faster processing times and improved communication throughout the application process.

Change Management and Organizational Adaptation

The transition to AI-driven loan processing represents more than a technological upgrade; it requires a fundamental shift in organizational processes and culture. Successful implementations have demonstrated the importance of:

Training and Skill Development: Staff must be equipped with new skills to effectively work alongside AI systems. This includes developing expertise in data analysis, AI system monitoring, and exception handling for complex cases that require human intervention.

Process Redesign: Existing workflows must be reimagined to take full advantage of AI capabilities while maintaining appropriate human oversight. This includes establishing clear escalation paths for complex cases and defining roles for high-value activities that benefit from human judgment.

Case Studies in AI-Driven Loan Processing

The transformative impact of AI in loan processing is best illustrated through real-world implementations across various financial institutions. These case studies demonstrate both the potential and practical considerations of AI adoption in lending operations.

Large National Bank Implementation

A leading national banking institution's implementation of AI-driven loan processing represents a benchmark in digital transformation within traditional banking. This institution, with over $100 billion in assets and a presence across multiple states, approached AI integration with a systematic methodology that yielded remarkable results:

Pre-Implementation Metrics (2022):

- Average processing time: 120 hours

- Manual review requirement: 85% of applications

- Error rate: 3.2%

- Customer satisfaction rating: 72%

Post-Implementation Metrics (2024):

- Average processing time: 4 hours

- Manual review requirement: 15% of applications

- Error rate: 0.3%

- Customer satisfaction rating: 94%

The success at this institution demonstrates the importance of a comprehensive implementation strategy that addresses both technical and organizational aspects of AI integration. Their approach particularly excelled in maintaining high accuracy while dramatically reducing processing times.

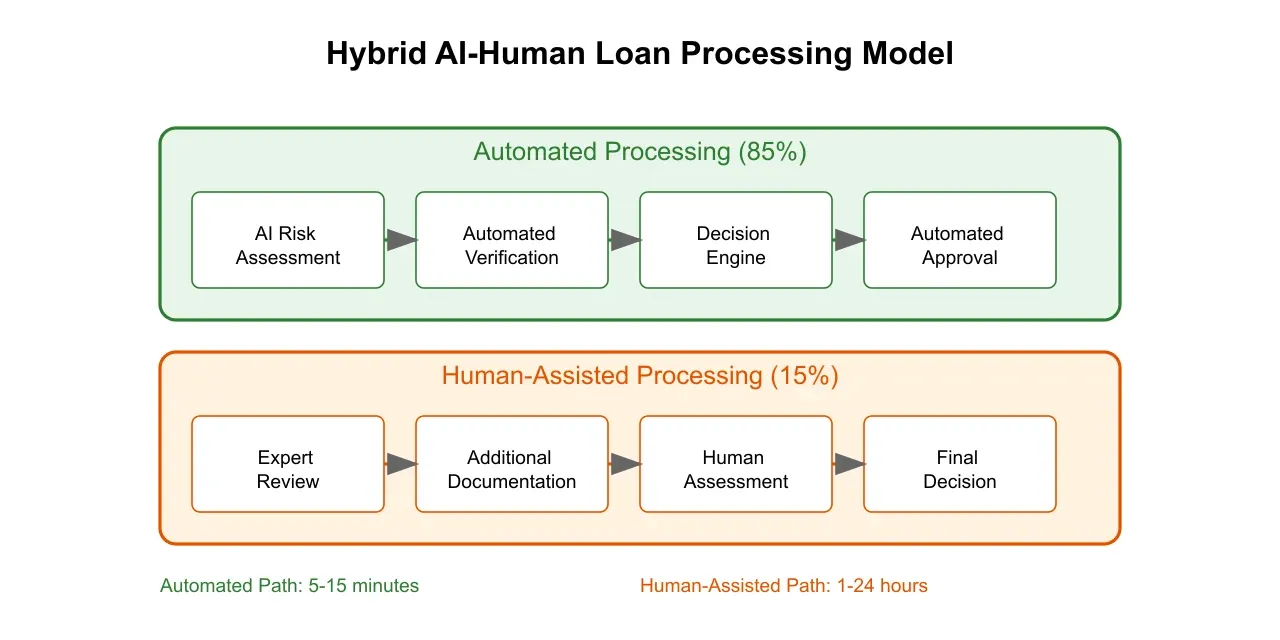

Regional Bank Transformation

A mid-sized regional bank's experience offers valuable insights into how smaller financial institutions can successfully implement AI-driven loan processing while maintaining their community-focused approach. Figure 4 illustrates their hybrid model that combines AI efficiency with personalized service.

The regional institution, serving a population of approximately 2 million across three states, achieved significant improvements while maintaining its strong community relationships:

- 70% reduction in routine processing tasks

- 45% increase in loan officer availability for complex cases

- 85% improvement in first-time approval accuracy

- 60% decrease in processing costs

Future Implications and Emerging Trends

The evolution of AI-driven loan processing continues to accelerate, with several key trends shaping the future landscape of lending operations.

Advanced Analytics and Alternative Data

The next generation of AI lending systems will incorporate an increasingly diverse range of alternative data sources to enhance credit assessment accuracy. These systems will analyze:

Social Media and Online Presence: While maintaining strict privacy compliance, AI systems will evaluate digital footprints to assess business stability and consumer behavior patterns. This analysis will be particularly valuable for evaluating thin-file applicants and small businesses.

IoT and Connected Device Data: For business loans, AI systems will incorporate real-time operational data from IoT devices to provide more accurate risk assessments and enable dynamic lending terms based on business performance metrics.

Behavioral Analytics: Advanced AI models will analyze applicant interaction patterns during the application process itself, providing additional insights into risk profiles and potential fraud indicators.

Quantum Computing Integration

The emergence of quantum computing capabilities promises to revolutionize AI-driven loan processing further. Quantum algorithms will enable:

Complex Risk Modeling: Quantum-enhanced AI will process vastly more variables simultaneously, creating more nuanced risk assessments that consider complex market interactions and economic scenarios.

Real-Time Market Analysis: Quantum computing will enable instantaneous analysis of market conditions and their potential impact on loan performance, allowing for truly dynamic risk assessment and pricing.

Regulatory Technology (RegTech) Evolution

The integration of AI in loan processing will continue to evolve alongside regulatory requirements, with several key developments on the horizon:

Automated Compliance Monitoring: AI systems will increasingly incorporate real-time compliance monitoring capabilities, automatically adjusting their operations to maintain alignment with evolving regulatory requirements.

Enhanced Transparency: Future AI systems will provide even more granular explanations of their decision-making processes, satisfying both regulatory requirements and growing demands for algorithmic transparency.

Conclusion

The transformation of loan processing through AI represents a fundamental shift in how financial institutions approach lending operations. The demonstrated success of early adopters, combined with continuing technological advances, suggests that AI-driven loan processing will become the industry standard within the next decade.

Financial institutions must carefully consider their approach to AI integration, balancing the promise of efficiency gains against the need for thoughtful implementation and robust risk management. Success in this transformation requires a comprehensive strategy that addresses technical infrastructure, regulatory compliance, organizational change, and customer experience.

As AI technology continues to evolve, institutions that successfully implement these systems will gain significant competitive advantages through improved efficiency, reduced costs, and enhanced customer satisfaction. The future of lending lies in the intelligent application of AI technologies, creating a lending ecosystem that is faster, more accurate, and more accessible than ever before.